Creditors spend millions keeping borrowers in the dark about Chapter 7 bankruptcy. They profit from your fear and confusion about the filing process.

We at Harnage Law, PLLC know what information creditors hope you never learn. This guide reveals the facts about Chapter 7 that protect your rights and finances in Florida.

What Chapter 7 Actually Eliminates

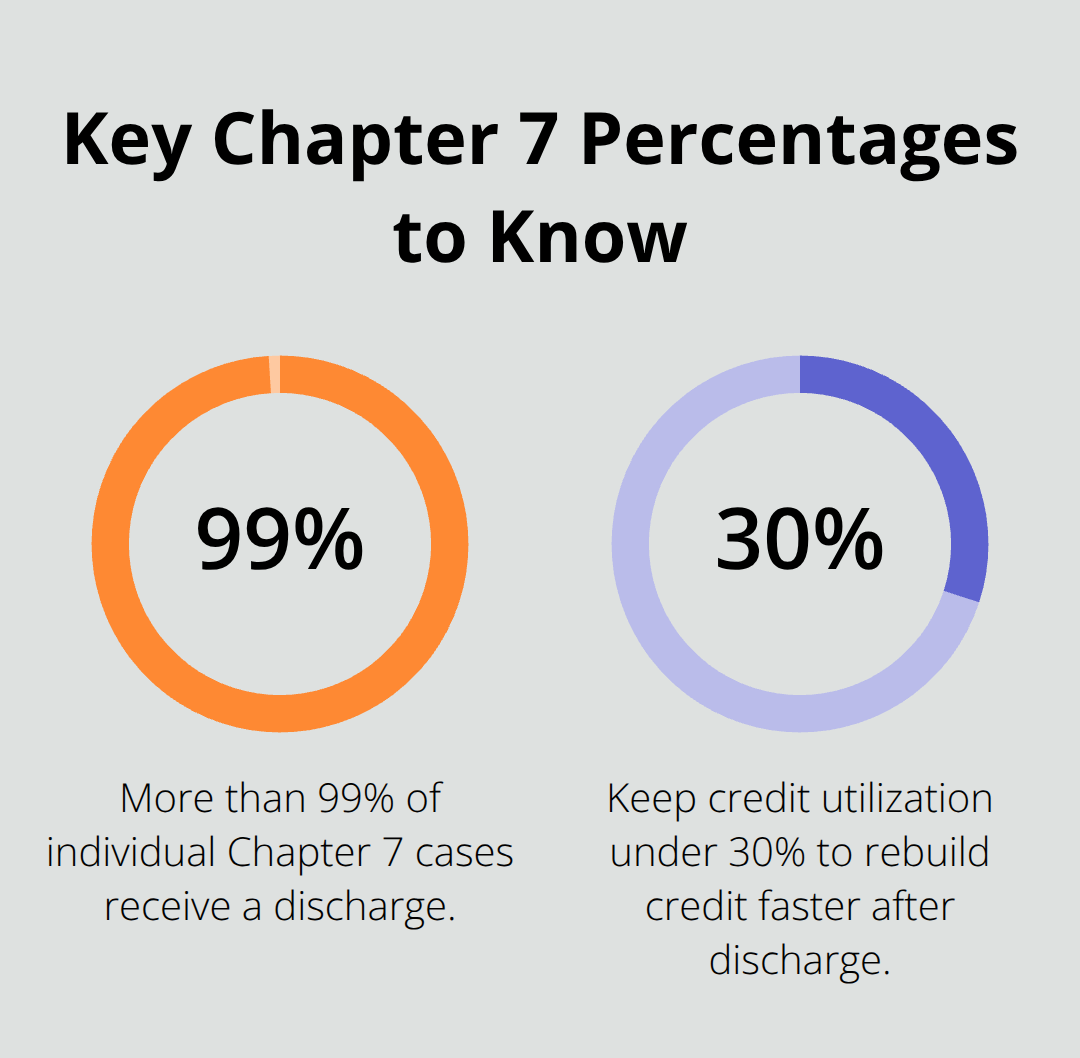

Chapter 7 bankruptcy discharges credit card balances, medical bills, personal loans, payday loans, back rent, and past-due utilities. These debts vanish through the discharge process, which typically occurs 60 to 90 days after your creditor meeting. Federal bankruptcy data shows that more than 99% of individual Chapter 7 cases result in a discharge, meaning the system works as intended for the vast majority of filers. The discharge is permanent and legally binding-creditors cannot pursue collection after the court issues the order.

If a creditor attempts to collect a discharged debt, you can reopen your case to enforce the discharge injunction, which may result in sanctions against them.

The Automatic Stay Halts Collection Immediately

The moment you file Chapter 7, an automatic stay takes effect and stops most collection actions within hours. Wage garnishments cease, collection lawsuits pause, and creditor phone calls must stop. This federal court order carries serious consequences for creditors who violate it. Creditors know this rule well, which is why the filing itself becomes your most powerful tool against harassment. Some collection actions fall outside the stay, such as criminal proceedings or certain family law matters, but unsecured debt collection stops cold. You gain relief immediately upon filing-not weeks later.

Foreclosure and Repossession Pause During the Stay

Chapter 7 does not permanently prevent foreclosure or repossession of secured property like homes or vehicles, but it does trigger the automatic stay, which forces lenders to pause their actions temporarily. During this window, you have options: you can reaffirm the debt to keep the property, work out a modification with the lender, or let the property go through the discharge process. If you own a home in Florida and want to keep it, Chapter 13 typically offers a better path because it allows you to catch up on back payments through a repayment plan. Chapter 7 buys you time and breathing room to assess your situation without creditors moving forward aggressively.

The protection Chapter 7 provides extends beyond stopping collection calls-it fundamentally shifts the power dynamic between you and your creditors.

What Florida Bankruptcy Law Lets You Keep

Your Home Receives Unlimited Protection Under Florida Law

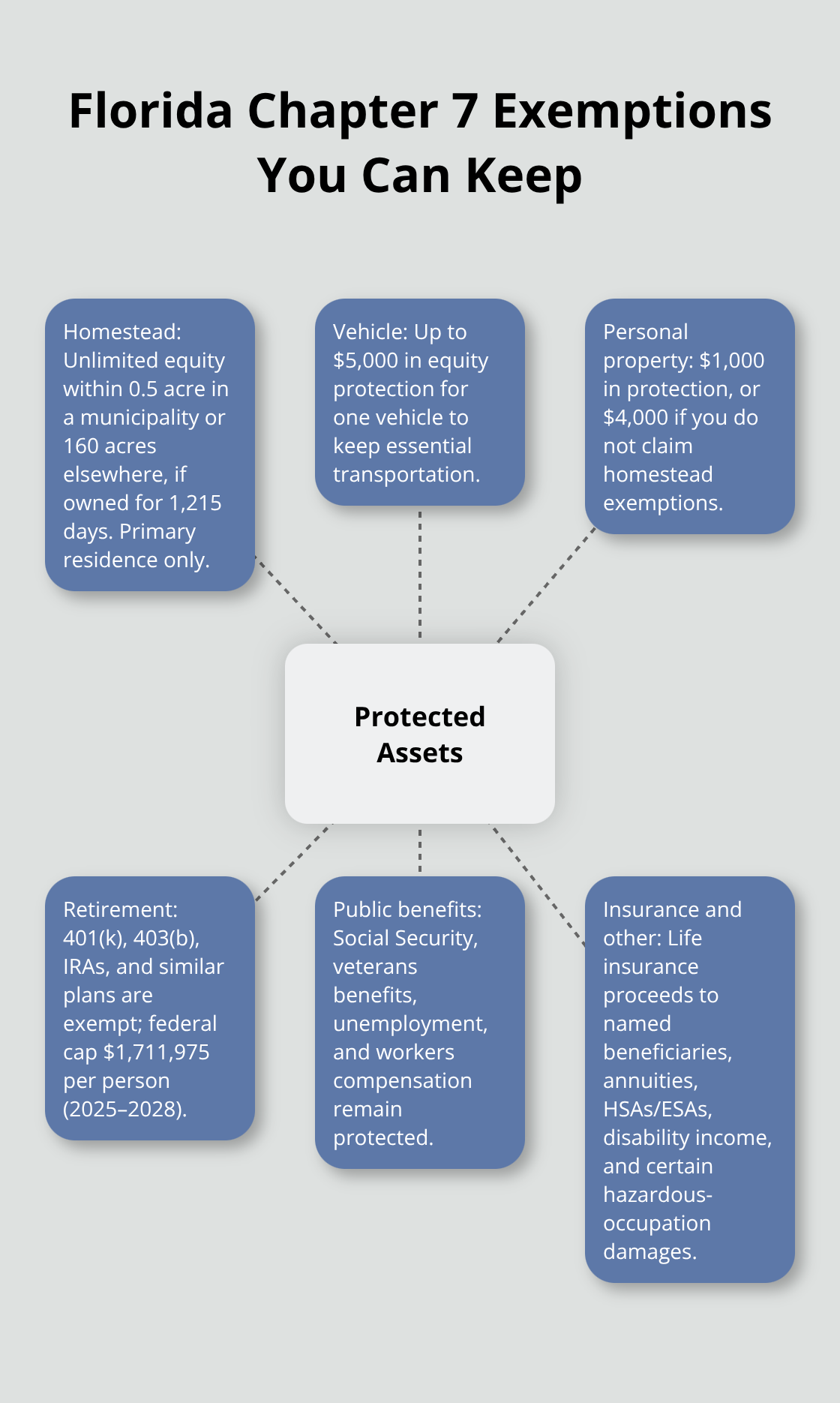

Florida’s exemption system differs dramatically from federal rules, and this difference protects substantial wealth for filers who understand it. Florida residents filing Chapter 7 can shield unlimited home equity within half an acre in a municipality or 160 acres elsewhere, but ownership must reach 1,215 days before filing-roughly three years and four months. If you fall short of this timeline, federal law caps your homestead protection at $214,000. This protection applies only to your primary residence, and the court will verify your ownership duration at the 341 meeting. The trustee cannot force a sale of your home to pay unsecured creditors, even if significant equity exists, provided you meet Florida’s residency requirement.

Vehicles and Personal Property Stay Protected

A single vehicle receives up to $5,000 in equity protection under Florida law, which covers most financed cars and keeps reliable transportation intact during the filing process. Personal property like furniture, electronics, and household items receive $1,000 in protection, or $4,000 if you do not claim homestead exemptions. These limits sound restrictive until you realize most household goods have minimal resale value, so the trustee rarely liquidates everyday belongings. The trustee must determine what property qualifies as nonexempt and whether liquidation would generate meaningful funds for creditors. In practice, most Chapter 7 filers retain their essential possessions without interference.

Retirement Accounts and Public Benefits Remain Untouchable

Retirement accounts face nearly complete protection in Florida Chapter 7 cases. Traditional 401(k)s, 403(b)s, IRAs, and similar qualified plans are exempt under both state and federal law, with a federal cap of $1,711,975 per person for filings between 2025 and 2028. Public benefits including Social Security, veterans benefits, unemployment compensation, and workers compensation cannot be touched by creditors or the bankruptcy trustee. Life insurance proceeds paid to a named beneficiary remain exempt, as do annuity payments and the cash surrender value of policies.

Additional Protected Income and Assets

Disability income, fraternal benefit society benefits, and alimony received for support of dependents all stay protected from creditors. Florida law also shields education savings accounts, health savings accounts, and prepaid medical savings from creditors. Damages from injuries or deaths in hazardous occupations receive exemption protection, though general personal injury settlements depend on the circumstances and applicable exemptions. After discharge, creditors lose all collection rights to these protected assets and cannot pursue them through garnishment, levy, or other means.

The Discharge Injunction Creates a Permanent Barrier

The discharge order itself becomes a permanent legal barrier preventing any creditor from attempting collection on discharged debts, and violating this injunction exposes creditors to court sanctions and potential damages. This protection extends to all assets you claim as exempt-creditors cannot circumvent the discharge by targeting protected property through alternative collection methods. Understanding which assets Florida law protects allows you to file with confidence that your essential financial foundation remains intact. The specific assets you retain depend on your circumstances, which is why reviewing your situation with a bankruptcy attorney helps clarify what you can keep and what the trustee may liquidate.

The Real Timeline and Cost of Chapter 7 in Florida

How Fast Chapter 7 Actually Moves

Chapter 7 bankruptcy in Florida moves faster than most people expect. From the moment you file until discharge, the entire process typically spans four to six months, though the timeline breaks into distinct phases that creditors rarely explain. The filing itself takes effect immediately, triggering the automatic stay within hours. Your creditor meeting, formally called the 341 meeting, occurs 21 to 40 days after filing.

The trustee and creditors can question you under oath about your finances and property, though in most cases the meeting lasts under ten minutes. After this meeting, a 60-day window opens for creditors and the trustee to object to your discharge. If no objections surface, the court issues your discharge order roughly 60 to 90 days after the creditor meeting.

Discharge Rates Show the Process Works

Federal bankruptcy data shows that more than 99% of individual Chapter 7 cases result in discharge, meaning the timeline holds steady for the vast majority of filers. This speed matters because every month of delay extends the period when creditors can still pursue collection, wage garnishment, and lawsuits against you. The faster you move through the process, the sooner creditors lose their collection rights.

Breaking Down the Three Cost Components

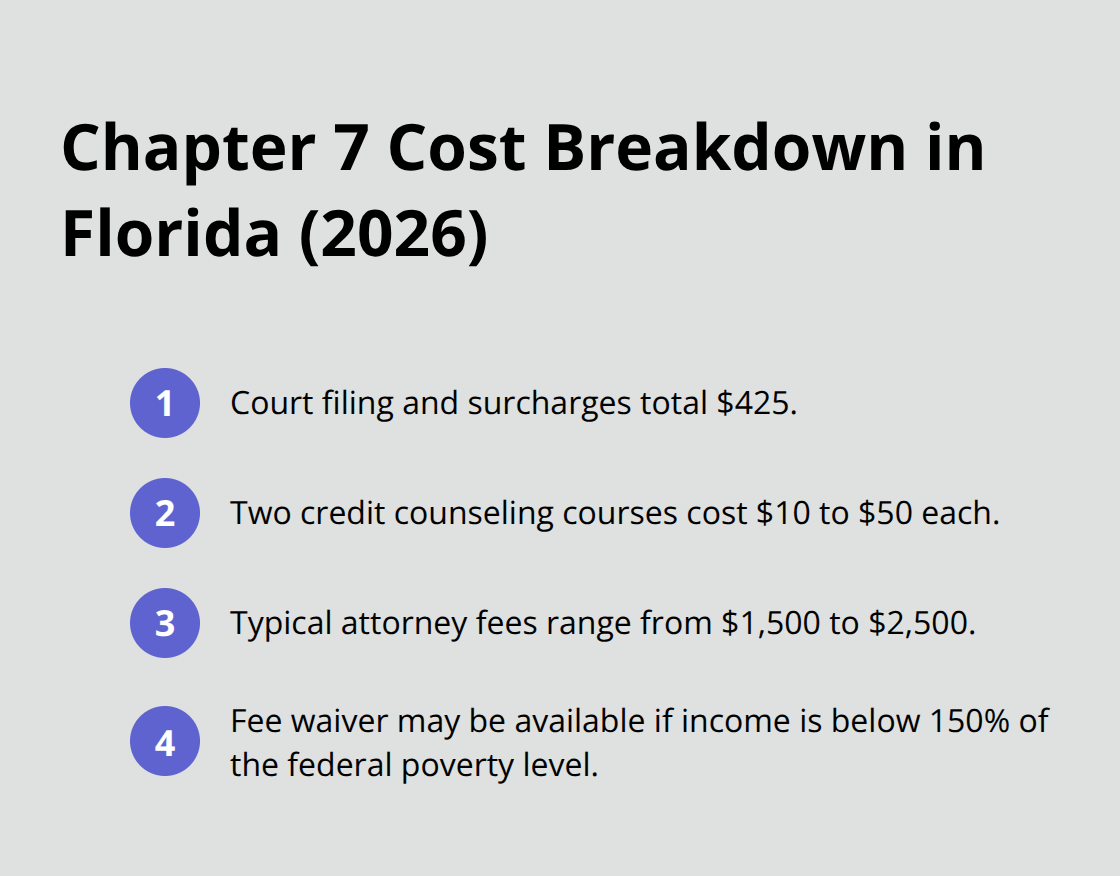

The actual cost of Chapter 7 breaks into three components: court filing fees, mandatory credit counseling courses, and attorney representation. Court filing fees total $335 as of 2026, plus a $75 administrative fee and a $15 trustee surcharge, bringing the total court cost to $425. If your income falls below 150% of the federal poverty level, the court may waive these fees entirely, though you must request a waiver when filing.

Credit Counseling and Attorney Fees

Two mandatory credit counseling courses add $10 to $50 each, depending on the provider. The largest expense comes from hiring a bankruptcy attorney. In Florida, Chapter 7 attorney fees typically run $1,500 to $2,500, with some firms offering payment plans to spread costs across multiple installments.

Why Filing Sooner Saves Money

Delaying your filing postpones these costs but extends the damage creditors inflict through garnishments, lawsuits, and harassment. Each month you wait costs you more in lost wages through garnishment and accumulated interest on debts that Chapter 7 would eliminate. Filing sooner rather than later preserves your income and stops the financial bleeding that makes your situation worse.

Final Thoughts

Discharge means creditors lose all legal right to collect on debts included in your Chapter filing. Once the court issues the discharge order, those debts vanish permanently, and creditors cannot pursue collection through lawsuits, wage garnishment, or any other method. This finality separates Chapter 7 from other options like debt consolidation or negotiated settlements, where creditors retain collection rights. The discharge covers credit cards, medical bills, personal loans, and similar unsecured debts that have burdened your finances.

Rebuilding credit after Chapter 7 starts immediately after discharge, and your credit score will drop initially but improves faster than many people assume. Secured credit cards, which require a cash deposit, help demonstrate responsible borrowing to credit bureaus. Keeping credit utilization below 30% on any accounts you open shows lenders you manage available credit responsibly, and services like Experian Boost let you count rent and utility payments toward your credit score, accelerating improvement without taking on new debt.

Moving forward without the burden of qualifying debts transforms your financial reality, as the freed-up income becomes available for essential expenses, savings, and rebuilding your financial foundation. The psychological relief of eliminating overwhelming debt often matters as much as the financial benefit. We at Harnage Law, PLLC guide clients through every step of the Chapter filing process and help them understand what discharge truly means for their financial recovery-contact us to discuss how Chapter 7 can provide the fresh start you need.